As of June 2022, a total of 2,090 Iowans have had $106.8 million in student loan debt forgiven at an average of $51,100 per borrower through the Public Service Loan Forgiveness (PSLF) Program. Temporary changes to the program could mean that you or someone you know may now qualify to have thousands of dollars in student loan debt forgiven.

“I initially didn’t qualify for the PSLF due to my student loan type,” said one Iowa borrower, “but now I am going through the process of having my remaining student loan debt forgiven within the next few months.”

About the Public Service Loan Forgiveness Program

The PSLF Program was created as part of the College Cost Reduction and Access Act that was passed by Congress and signed into law by President George W. Bush in 2007. The intent of the program is to encourage students to enter and sustain careers in service to the public. The incentive was that after 10 years of making qualifying monthly payments, a borrower’s remaining student loan debt would be forgiven. Here were the original general rules in order to qualify:

- Be a full-time employee of a qualifying employer;

- Make 120 qualifying on-time monthly payments; and

- Make payments on eligible student loans

Qualifying Employer. Qualifying employers were limited to government (local, state, federal, tribal, and U.S military); nonprofit entities with a 501(c)(3) tax exemption; nonprofits without a 501(c)(3) tax exemption but providing qualifying public services; and/or contractors doing work under a qualified employer. Full-time volunteers with AmeriCorps and Peace Corps also qualify. Full-time work is generally considered at least 30 hours per week or more. Part-time workers with a combined 30 hours or more per week of work with qualified employers are also eligible. 120 Monthly Payments. The original program required 120 on-time monthly payments in one of two approved repayment plans: the standard plan or the income-driven plan. While the standard plan provided qualifying payments, to benefit from the program participants would need to switch to an income-driven repayment plan. Payments made while in school, in deferment, or in forbearance did not qualify.

Eligible Student Loans. The only student loans eligible were those from the William D. Ford Federal Direct Loan (Direct Loan) Program.

PSLF Limited Waiver Opportunity

In October 2021, the Department of Education announced temporary updates to the PSLF Program that qualified millions of additional public service workers for loan forgiveness. Until October 31, 2022, past payments and loan types that were previously ineligible for forgiveness may become eligible if the borrower completes the steps necessary to make their loans qualify.

Payments. For a limited time, past periods of repayment that would not have originally qualified—such as no or partial payments, deferment, forbearance, and more—may now qualify as payments toward the 120 monthly payments that are necessary. Those who have complete 120 or more monthly payments, may have their remaining loan debt forgiven. Those who have not completed 120 months of payments may continue towards forgiveness if they follow the steps below.

Eligible Student Loans. Federal Family Education Loans and Federal Perkins Loans may become eligible if the borrower consolidates them into a Direct Consolidation Loan before the end of October 2022. You should note that if the borrower has not already reached the 120-month requirement for forgiveness during this waiver period, further payments due on these newly consolidated loans must be made as part of an income-driven repayment plan versus a standard repayment plan to continue qualifying payments toward loan forgiveness.

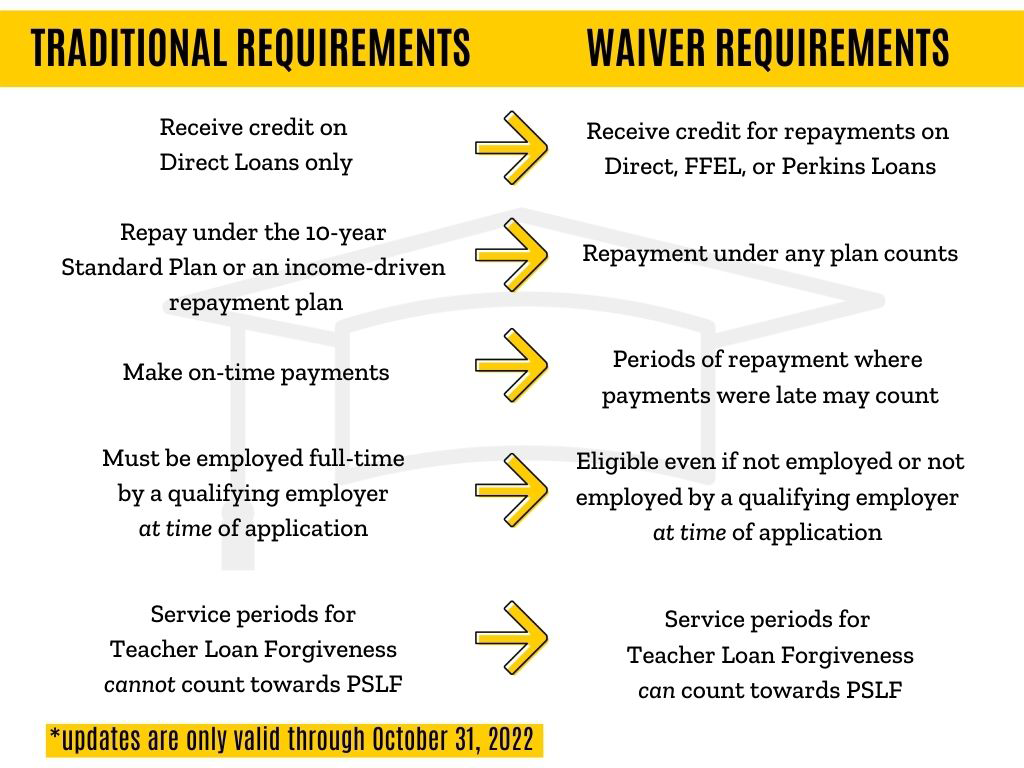

The chart below outlines the traditional PSLF requirements in comparison to the updates that will be in place until the end of October.

How to Apply

With the October 31 deadline fast approaching, it’s important to start taking advantage of the temporary waiver now.

“[The process] takes forever. It’s not a two-week turnaround. There could be a 30-, 60-, or 90-day timeframe on the whole process,” said one borrower.

STEP 1: See if you qualify. Create an account through the Department of Education’s website. Once you are into your account, you should be able to view loan type(s), loan amount(s), and who is servicing your loan(s) by looking at your “Dashboard” page found under the person icon in the upper-right corner of the website.

STEP 2: See if your employer(s) qualify. Again, the Department of Education has a website for you to search qualifying employers by their Employer Identification Number (EIN). You should find the EIN on your Wage and Tax Statement (W-2). Then go to the page Search Employer Eligibility for Public Service Loan Forgiveness (PSLF). Even though you have not worked for a qualifying employer in the past, you may still consider this program if you think you may work for a qualifying employer for 10 or more years in the future.

STEP 3: Consolidate your loans. If your loans are not already Direct Loans or Direct Consolidation Loans—but are FFEL or Perkins Loans—you will need to consolidate your loans into a Direct Consolidation Loan. You can follow the steps to do that on the Student Loan Consolidation page. If you’ve already made 120 or more qualifying payments, your loans may be considered for immediate forgiveness.

STEP 4: Submit a PSLF Certification & Application. From your Department of Education account, you may select the “Manage Loans” tab and then select “Public Service Loan Forgiveness” option. There the “PSLF Help Tool” will help you generate the correct document. Again, you will briefly go through employer eligibility, as well as loan and repayment eligibility. Then—depending on whether you have made120 qualifying payments or a lower number of payments—the system will generate a document. From there, you will do the following: (a) download and print the form; (b) read and sign the form; (c) have your employer read and sign the form; and (d) either upload, fax, or mail the form as instructed.

PSLF Impact on Iowans

According to Bureau of Labor Statistics data, as of May 2022 Iowa has a civilian workforce of approximately 1.7 million people. Iowans employed in local, state, and federal government number around 257,000 and those employed at a 501(c)(3) tax-exempt nonprofit organization number around 190,000 . When added together, that means an average of 1 in 4 Iowans work for a qualified employer for the PSLF program.

One eastern Iowan with two professional degrees in law and business has worked for public and nonprofit employers focused on education for nearly her entire career. After 17 years of regular student loan payments, the temporary changes to PSLF qualified her remaining $50,000 in student loan debt to be forgiven. “I was denied originally because of a consolidation issue. My loans were just in the wrong place,” she says. While she has been offered higher paying positions from other employers, she was willing to carry the financial burden of student loan debt to continue to work in public service. “[Education] is how we can change the future of Iowa through students and services for the state. We need to help people afford to work in nonprofits.”

A current employee at a central Iowa social services organization holds both undergraduate and graduate degrees in social work. While her loans have not yet been forgiven, she has filed the necessary paperwork and is potentially just months away from forgiveness through PSLF.

“If my loans are forgiven, over $100,000 will be taken off my plate. I don’t think I’d ever otherwise be able to repay my loans without this program,” she says. Even though her public service work spans all the way back to high school, the PSLF program heavily influenced her decision to pursue her degrees and build a career in nonprofits. “The people that this program benefits provide mission-driven and critical work. So many people directly and indirectly benefit from this program. Of course, the individuals who have their loans forgiven benefit, but the individuals who receive help from nonprofit organizations also benefit.”

“There is no way I could have become a health care professional without my undergraduate and professional education,” added a rural western Iowan whose been making student loan payments since 2006. He continued, “And even though I had scholarships, I also needed student loans.”

How You Can Raise Awareness of this Limited Opportunity

The subject of student loan debt can be a sensitive one, so the topic is oftentimes avoided by employers and employees. We don’t want lack of communication to mean that hundreds or thousands of eligible Iowans miss this opportunity. The eligible borrowers we spoke to found out about the program in different ways. Some learned about it from colleagues while others were alerted through their current loan servicers.

“I did not know I was eligible,” said one borrower, “I received a letter from my loan servicer that I may be eligible for this program.”

“This program just isn’t communicated well enough. I didn’t even know PSLF existed until I heard about it through a friend. Many of my colleagues heard about it through word of mouth as well.”

One way to raise awareness is to share this article with individuals who may qualify for PSLF or even leaders of qualifying employers. Time is running out, so please share this information now.

Finally, if you have had—or are in the process of—benefiting from the PSLF Program, let us know by taking our survey. The survey results will provide valuable information about Iowans in public service.

Sources:

U.S. Department of Education:

Federal Student Aid: Public Service Loan Forgiveness Data

Federal Student Aid: Public Service Loan Forgiveness (PSLF)

U.S. Bureau of Labor Statistics: